Data Driven

Funding drivers are based on key metrics that align with UC Irvine's strategic plan to support well-informed, data-driven decision making.

Predictable

Campus planning assumptions are shared and projected resources can be modeled to establish a clear rationale for budgets and greater predictability.

Transparent

More information and data is provided to improve transparency in decisions and strategic direction.

Holistic

All funds multi-year planning provides a more holistic perspective, highlighting opportunities to leverage non-core sources to support strategic goals.

Address Funding Gap

These goals combined with budget principles work towards building a comprehensive plan for addressing the funding gap.

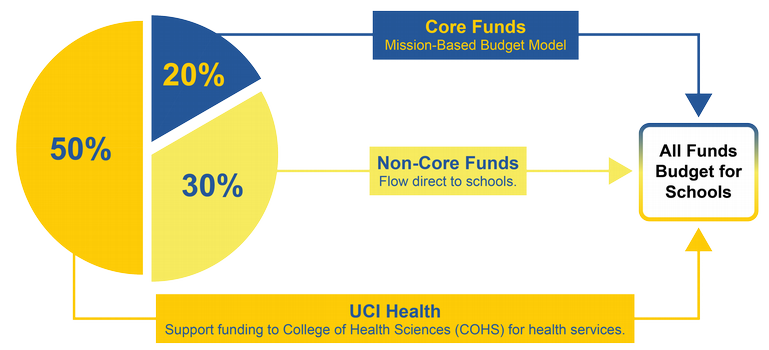

All Funds Overview

UC Irvine’s operating budget is over $6 billion and is supported by a variety of funding sources. The mission-based model focuses on core funds. To effectively manage operations, schools must consider all available resources—not just core funds. Additional funding sources may include contracts & grants, clinical revenues, philanthropy, and more. The graphic below provides a high-level overview of how core and non-core funds impact planning. For a full breakdown of UC Irvine’s funding sources and how they support the university’s operations, visit the Financial Stability Plan webpage.

All Funds Operating Budget

Funds Flow to Schools

The mission-based budget model allocates core funds to schools that are distributed based on key drivers that reflect faculty investments, student instruction and services, and research activity.

The model is not solely intended to support activities tied to the specific metrics; rather, it provides a framework for determining the total core resources available to each school. Within the context of overall campus goals, schools are responsible for establishing school-level budgets that reflect their unique strategies, priorities, and costs. Decisions on fund distribution to departments are best made by school leadership and other stakeholders based on the needs and goals of the individual schools.

Click the boxes below for more information. For the best experience, use Chrome or Firefox.

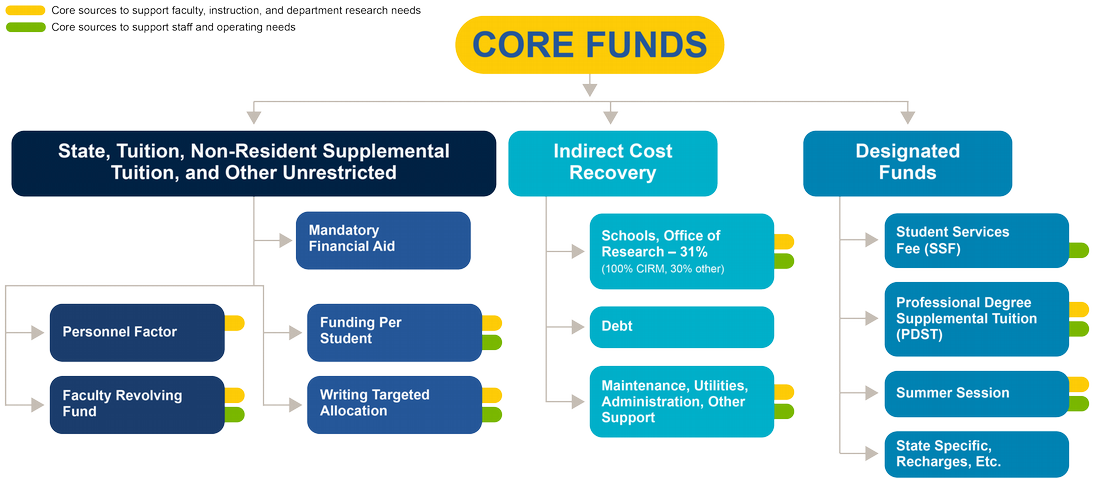

Core Funds

Core funds support the university's core mission of teaching, research, and public service and are comprised of tuition and fees, the state appropriation, indirect cost recovery, investment earnings, other unrestricted resources, and funds designated for specific programs.

State, Tuition, Non-Resident Supplemental Tuition, and Other Unrestricted

Annual State of California appropriation (see the California State Budget), tuition, non-resident supplemental tuition (NRST), and other unrestricted resources (e.g. investment earnings, general and administrative assessment, ground lease revenues).

Mandatory Financial Aid

In accordance with Regents Policy 3101, a portion of tuition and nonresident supplemental tuition revenue is reserved for need-based student financial aid, a practice called return-to-aid (RTA).

Personnel Factor

Together with the funding per student factor and the faculty revolving fund, the personnel factor provides a base campus investment in support of the teaching, research and service mission. The faculty investment factor is defined as 70% of each school’s average faculty salary and benefits; this amount is one contributor to covering the cost of faculty / staff / operating needs with the remaining costs covered through other components of the mission-based budget model (e.g., student metric-based, designated sources, ICR, non-core sources).

The calculation is as follows:

Budgeted faculty full time equivalent (FTE) × (average school S&B) * 70%

The data used is per the December snapshot of budgeted FTE and salaries. Benefits are calculated at Composite Benefit Rates (CBR). More information on CBR is available at Accounting & Fiscal Services website and Office of Research website.

Faculty Revolving Fund

Incremental allocations representing open faculty position funding and other strategic faculty investments, calculated as follows:

Initial allocation ± increments1 = ending balance.

1Increments include merits, promotions, new campus-funded FTE, funding withdrawals on separation, transfers to/from other schools.

Funding per Student (Instruction & Operating)

School-specific rate × weighted student FTE.

The school-specific rates per student were established to recognize that the cost of instruction varies from one discipline to the next. The differential rates were established based on an analysis of two factors: prior budget levels as a proxy for instructional needs and benchmark data from a national study on instruction costs by discipline. Each school’s respective rate per weighted student FTE will be adjusted each year to reflect core funding factors like tuition rate increases and state funding changes.

Weighted student FTE are calculated as follows:

- 2-year rolling averages for both student credit hour and enrollment data based on prior year and current year fall data converted to 3 term average (3TA) estimate.

- Degree data is based on the rolling average of the prior two years. Degrees are measured from Fall through Summer.

- Student credit hours (SCH) are based on the payroll home department method where credit is attributed to the home department of the instructor.

- The calculations to convert SCH to FTE are:

- undergrad: annual SCH ÷ 45

- grad (excluding law): annual SCH ÷ 36

- law (on semesters): annual SCH ÷ 24

- Student metrics are weighted as follows:

- 80% student credit hours (SCH)

- 10% enrollment

- 10% degrees granted

$ per student are the same for undergraduate and graduate students.

Writing Targeted Allocation

An annual allocation per student FTE is provided and inflation adjusted each year. Student FTE is calculated based on the projected number of composition and academic English sections times units per course and multiplied by estimated enrollments to determine student credit hours (SCH). SCH are divided by 45 to convert to FTE.

Indirect Cost Recovery (ICR)

Funds generated as a result of research expenditures that help cover costs for maintenance, utilities, administration, and other research-related support.

Debt

Financing to fund university capital projects. Indirect cost recovery from grants and contracts is used to fund debt repayment for academic/research buildings.

Schools, Office of Research

Schools and the Office of Research receive 30% of their indirect costs (IDC) related to research managed in their respective units. Grants from the California Institute of Regenerative Medicine (CIRM) are an exception in that administrative funds flow directly to the Stem Cell Center and facilities funds are allocated directly to maintenance and utilities of affiliated space.

Maintenance, Utilities, Administration, Other Support

Maintenance, utilities, administration, and other support are costs that are unallowable as direct expenses on grants and contracts but are essential in sustaining and supporting the research enterprise.

Designated Funds (State specific allocations, program-specific student fees)

Targeted allocations from the state (e.g., student academic preparation and educational partnerships (SAPEP) outreach programs, basic needs, student mental health, financial aid, etc.), professional degree supplemental tuition (PDST), student services fee (SSF), and summer session.

Student Services Fee (SSF)

A mandatory systemwide fee for all registered students, used to support co-curricular programs, activities, and services that complement the academic experience.

Professional Degree Supplemental Tuition (PDST)

Additional amount paid by students enrolled in professional degree programs to support instruction and specifically to sustain and enhance program quality. The charges vary by program.

Summer Session

Summer Session is an opportunity for schools to offer and for students to take courses outside of the normal fall, winter, and spring quarters of the academic year. These might be strategic offerings of high demand courses or opportunities for students to complete requirements more quickly. A portion of net revenues is distributed to schools offering the courses.

State Specific, Recharges, Etc.

State specific allocations are targeted allocations from the state to fund student academic preparation and educational partnerships (SAPEP) outreach programs, basic needs, student mental health, financial aid, etc.

Recharges are costs charged to a university department, unit, activity, or project for specific goods or services provided by another university department/unit/activity/project.