Updated Nov. 17, 2025

Understanding UC Irvine’s Financial Landscape

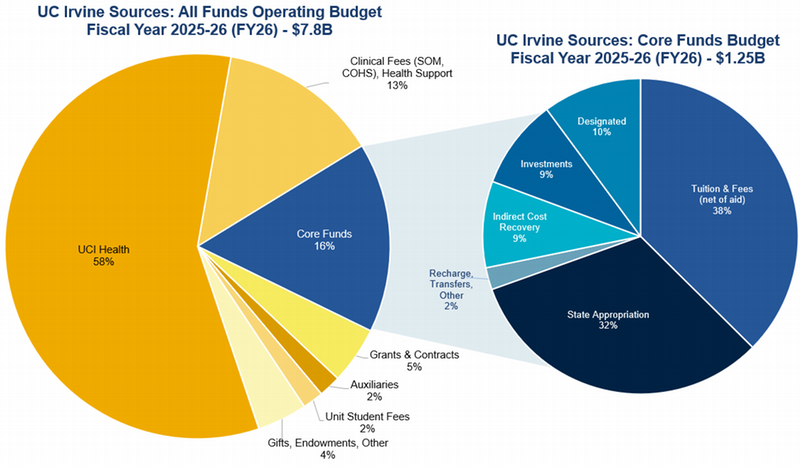

UC Irvine’s 2025-26 all-funds operating budget is $7.8 billion. Approximately half of the budget is attributed to UCI Health and its patient care services. Another third comes from non-core funds such as auxiliary units (like housing and parking), contract and grant expenditures, and health-related income that goes to the campus. The remaining funds, around $1.25 billion, are known as core funds and are the main focus of the financial stability plan. A description of each core and non-core fund source is provided here.

Financial Forecast

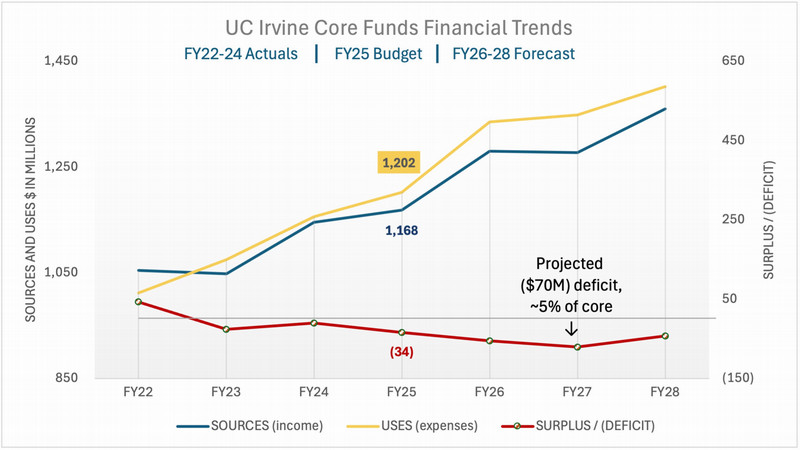

UC Irvine is facing a core funds structural deficit due to the fact that uses of funds have been increasing at a faster rate (5-8% per year) than sources of funds (1-4% per year). The current multi-year financial forecast includes actual sources and uses for FY23-FY25, the approved budget for FY26, and projections for FY27-FY28.

A plan has been established to address the remaining projected structural funding gap, defined in fall 2024 as $70 million, or about 5% of the core funds budget. This budget forecast is encouraging on paper, but financial stability depends on successful execution across all units as most schools and divisions still face structural deficits as captured in the orange shaded area showing the projected deficit if unit savings plans are not realized.

We are committed to transparency and will update this page annually in fall and as new information becomes available.

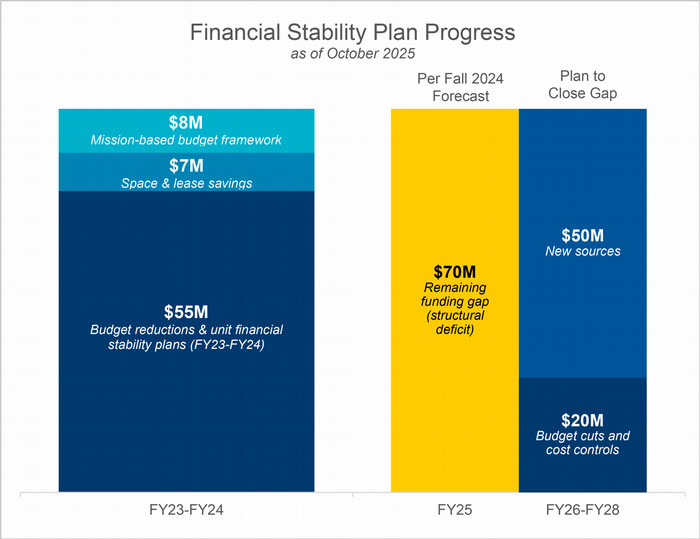

Tracking Our Progress

The graphic illustrates UC Irvine’s progress in addressing its structural deficit. From FY23–FY25, significant advancements were made through budget reductions, unit financial stability plan actions, space and lease cost reductions, and budget reallocations aligned with the mission-based budget model.

This progress reflects the collective efforts and dedication of the campus community in addressing the funding gap. Ongoing achievements demonstrate a commitment to fiscal responsibility by identifying new funding sources, leveraging non-core resources, and improving operational efficiency.